Investing is one of the most effective ways to build wealth over time, but choosing the right investment approach can significantly impact your financial journey. One of the most common questions among investors is “SIP vs Lump Sum: Which is Better?” Both methods have their own advantages and are suitable for different financial situations and market conditions. Understanding the differences between SIP and Lump Sum investing can help you make informed decisions and maximize your returns.

In this article, we will explore SIP vs Lump Sum: Which is Better?, their benefits, drawbacks, and the situations where each investment strategy works best.

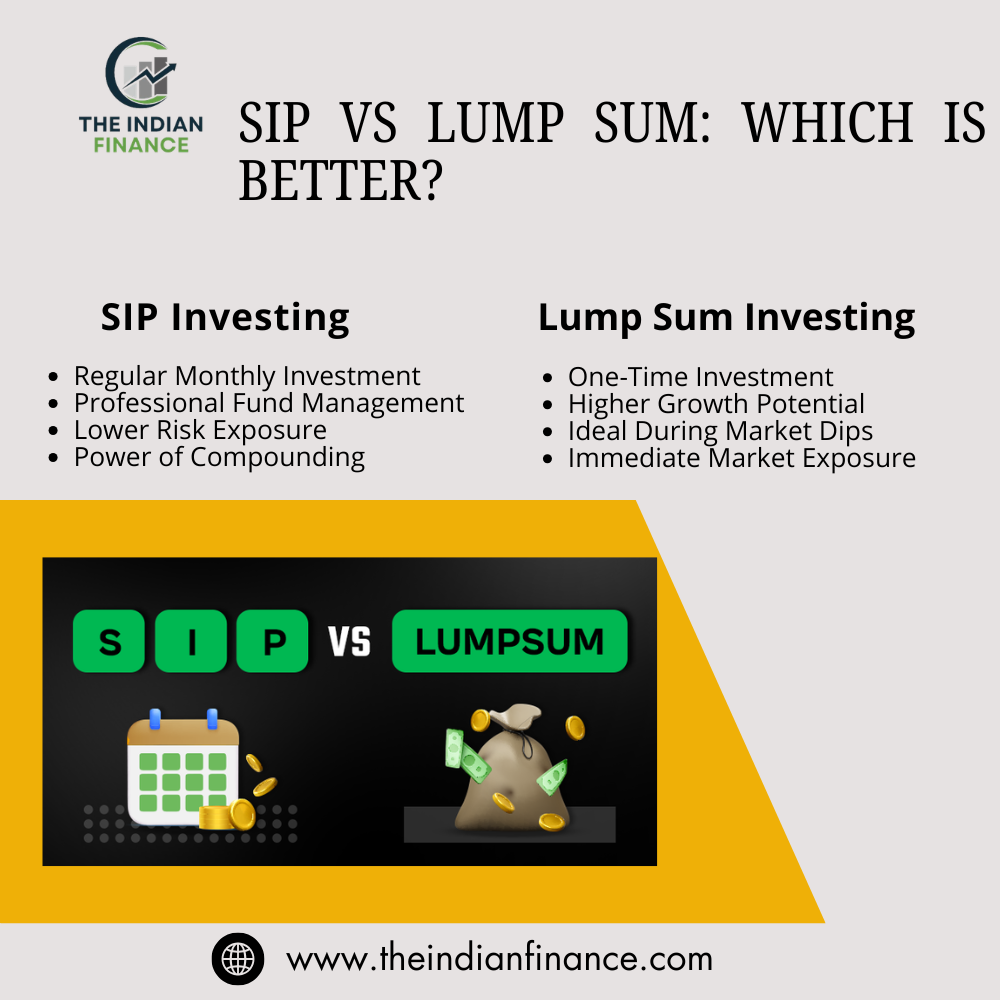

What is SIP?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly in mutual funds. Investors can choose to invest weekly, monthly, or quarterly based on their financial goals and income.

SIP allows individuals to invest consistently without worrying about market timing. It promotes disciplined investing and helps build wealth gradually over the long term.

When discussing SIP vs Lump Sum: Which is Better?, SIP is often preferred by salaried individuals because it aligns with their regular income pattern.

What is Lump Sum Investment?

A Lump Sum Investment involves investing a large amount of money at one time into a mutual fund or other investment instrument.

This approach is suitable for investors who have surplus funds from bonuses, inheritance, business profits, or savings. Instead of investing gradually, the entire amount starts working in the market immediately.

Understanding the concept of Lump Sum investing is essential when evaluating SIP vs Lump Sum: Which is Better?

Key Differences Between SIP and Lump Sum

| Factor | SIP Investment | Lump Sum Investment |

|---|---|---|

| Investment Mode | Regular, periodic contributions | One-time investment |

| Market Timing | Reduces risk through rupee cost averaging | Requires precise market timing |

| Risk Exposure | Lower due to phased investments | Higher due to market fluctuations |

| Compounding Benefits | Gradual accumulation over time | Full capital benefits from the start |

| Ideal For | Salaried investors, long-term wealth planning | Investors with surplus cash and high-risk appetite |

| Discipline | Encourages regular savings | One-time decision, no periodic tracking |

| Best Market Condition | Volatile or bear markets | Bull markets or undervalued markets |

SIP vs Lump Sum: Which is Better for Beginners?

For beginners, SIP is generally considered a safer and more comfortable investment option.

Advantages of SIP:

- Requires small investment amounts

- Encourages disciplined investing

- Reduces market timing risk

- Benefits from rupee cost averaging

- Suitable for long-term wealth creation

Many new investors choose SIP because they can start with a modest amount and gradually increase investments as their income grows.

When analyzing SIP vs Lump Sum: Which is Better?, SIP often wins for beginners due to its simplicity and lower risk exposure.

Benefits of Lump Sum Investing

While SIP offers gradual investment, Lump Sum investing provides immediate market exposure.

Advantages of Lump Sum:

- Entire amount starts earning returns immediately

- Potential for higher returns during bull markets

- Suitable for investors with available capital

- Simpler one-time investment process

- Ideal for long-term investment horizons

If the market is undervalued and expected to rise, a Lump Sum investment may generate higher returns compared to spreading investments through SIP.

This factor plays an important role in determining SIP vs Lump Sum: Which is Better?

SIP vs Lump Sum: Which Gives Better Returns?

The answer is not black and white. It depends on market conditions and your investment horizon:

| Scenario | Better Option | Reason |

|---|---|---|

| Volatile Market | SIP | Rupee cost averaging reduces risk |

| Bull Market (Rising) | Lump Sum | Full capital benefits from growth |

| Bear Market (Falling) | Lump Sum | Buy more units at lower NAV |

| Long-Term (10+ years) | Both work | Historical data shows 2-3X returns for both |

| Short-Term (<3 years) | SIP | Lower risk of timing the market wrong |

Historical Data: Lump sum investing typically outperforms SIPs over a 10- or 15-year horizon, delivering roughly 2- to 3-fold returns according to past data.

When Should You Choose SIP?

Choose SIP if:

✅ You want to reduce market volatility risk

✅ You prefer a disciplined investment approach

✅ You have a consistent income flow (salaried)

✅ You aim for long-term wealth creation through compounding

✅ You’re a beginner investor

✅ You cannot time the market

When is Lump Sum Investment Better?

Choose Lump Sum if:

✅ You have a large surplus fund available (bonus, inheritance, maturity)

✅ Markets are at a lower valuation with potential growth ahead

✅ You want to maximize capital growth from the start

✅ You’re comfortable with short-term market fluctuations

✅ You have high-risk appetite

✅ You can time the market wisely

SIP vs Lump Sum: Quick Decision Guide

| Your Profile | Best Choice |

|---|---|

| Salaried employee | SIP |

| Business owner with irregular income | SIP + Occasional Lump Sum |

| Have ₹5-10 lakhs surplus | Lump Sum (or STP from lump sum to SIP) |

| Beginner investor | SIP |

| Experienced investor | Both (based on market conditions) |

| Retired person | Lump Sum (conservative funds) |

| Young professional | SIP |

| Market at all-time high | SIP |

| Market at correction/dip | Lump Sum |

Smart Strategy: Combine Both (STP Method)

A blended strategy combining SIP and lump sum can optimize wealth creation while balancing risk:

How it works:

Invest a large amount as Lump Sum in a Liquid Fund

Set up STP (Systematic Transfer Plan) to transfer fixed amounts monthly to Equity Fund

This gives you benefits of both strategies

Benefits:

Reduces timing risk

Earns interest while waiting to invest

Disciplined approach like SIP

Risks of SIP and Lump Sum Investing

Every investment strategy carries risks.

SIP Risks:

- Lower returns during rapidly rising markets

- Requires long-term commitment

- Returns depend on market performance

Lump Sum Risks:

- High exposure to market timing

- Greater short-term volatility

- Potential losses if invested at market peaks

Investors should carefully assess risk tolerance before deciding between SIP and Lump Sum.

Conclusion

When it comes to SIP vs Lump Sum: Which is Better?, there is no universal answer. SIP is ideal for investors seeking disciplined, low-risk, and long-term wealth creation, while Lump Sum investing can offer higher returns when invested at the right market conditions. The best strategy depends on your financial situation, investment goals, and risk tolerance.

Many successful investors combine both approaches to maximize opportunities while managing risk effectively. Instead of focusing solely on SIP vs Lump Sum: Which is Better?, focus on staying invested, maintaining discipline, and aligning your investments with your long-term financial objectives.

🚀 Start Trading Today – Open Your FREE Demat Account!

Option 1: Open Free Demat Account with Zerodha

Open a free demat account with Zerodha and start investing in stocks, derivatives, mutual funds, ETFs, bonds, IPOs, and more.

✅ Open Free Zerodha Demat Account

Option 2: Open Free Demat Account with Upstox

Looking for one app, one account to build your wealth? Join Upstox, loved and trusted by 1 cr+ Indians.

Open your account using our link within 7 days and enjoy:

🛒 Stock like you shop

💸 Buy Top Funds & Insurance

📰 News & expert insights

📈 Pro Mode to trade in F&O

Disclaimer

Disclaimer: This article is intended for educational and informational purposes only and should not be considered financial or investment advice. Mutual fund investments are subject to market risks. Investors should carefully read all scheme-related documents and consult a qualified financial advisor before making any investment decisions. Past performance is not indicative of future results.

Recommended Books

- The Intelligent Investor

- Rich Dad Poor Dad

- The Psychology of Money

- Common Stocks and Uncommon Profits

These books can help investors better understand wealth creation, risk management, and long-term investing principles.